As price inflation erodes confidence in the product, and a younger generation redefines what status actually signals, five structural shifts are forcing the world’s most prestigious brands to confront a question they have long deferred, not what they sell, but what transformation they genuinely deliver.

Nobody is lamenting the cost of living anymore. At a certain point, sustained inflation stops feeling like a crisis and starts feeling like the baseline, something to be absorbed and navigated rather than waited out. Prices are higher—they are not coming down—and consumers, across every category, have quietly recalibrated their expectations of what their money is actually worth.

In luxury, that recalibration has been particularly brutal. The pandemic years produced one of the most extraordinary consumption booms the sector had ever seen, with travel shut down, social life suspended and disposable income with nowhere obvious to go, high-net-worth consumers turned to objects. Handbags. Shoes. Watches. The major fashion houses reported results that defied economic logic (“revenge spending mentality”), and the conventional wisdom of the moment was that luxury had become, effectively, recession-proof.

It was a seductive conclusion. It was also wrong.

By 2024, the picture had reversed with an abruptness that caught many in the industry off guard. LVMH reported its first revenue decline in years. Kering saw profits fall by nearly half. Burberry issued a profit warning and suspended its dividend. Richemont and Tapestry both flagged weakening demand in key markets. The pandemic boom, it turned out, had not been a signal of luxury’s permanence. It had been a distortion, a displacement of spending that would have gone elsewhere, temporarily rerouted into goods. When normalcy returned, so did the question that had always been there: what is this actually worth?

What makes this moment genuinely interesting, rather than simply a familiar story of cyclical correction, is what is not in decline. While the major fashion houses absorbed the slowdown, the experience economy held, and in several categories, accelerated. Deloitte’s 2026 Global Powers of Luxury report found that 36.2% of executives now identify luxury travel as the sector with the highest growth potential, ahead of jewellery and ahead of fashion. The broader hospitality and high-end experience market has absorbed what goods could not retain—the desire to spend meaningfully on something that feels, in the most direct sense, worth it.

At a recent BTB Breakfast Briefing event held with industry decision-makers to unpack the latest intelligence insights in Asia-Pacific and Middle Eastern luxury (held under Chatham House rules), senior leaders from some of the world’s largest hotel brands, luxury communications practices and specialist consultancies sat with that question at the centre of the table. What is driving the divergence? What does the experience economy understand that product-led luxury has, for now, lost? And what does it demand of brands that intend to hold that ground?

Five key trends have emerged.

The Reset: Forces Reshaping the Market

Before examining where luxury is going, it is worth understanding why the departure from its previous logic has been so pronounced.

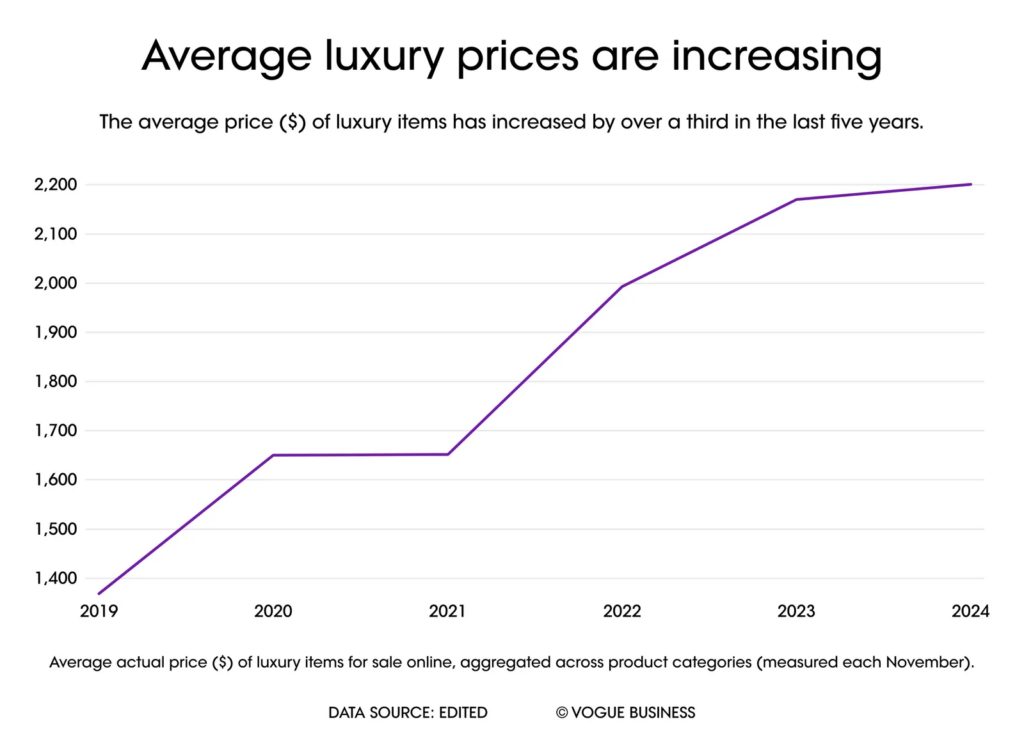

The first pressure is economic. Prices across luxury goods categories have risen by roughly 30 to 40% since 2022. For a sector that has always commanded a premium, this would ordinarily be unremarkable. What is different now is that consumers are increasingly unable to reconcile those price points with what they perceive as a decline in genuine distinctiveness. The emotional contract between brand and buyer —built on the promise that a higher price reflects something meaningfully superior—has been tested in ways that some brands have not recovered from.

The second is a shift in how status is communicated. In a culture mediated by digital imagery, a physical object flattens into a photograph. An experience generates something more durable: a story, a memory, a form of social currency that a static image cannot replicate. Access, be it to a place, a community, or a moment, has become a more legible signal of discernment than ownership.

The third is harder to quantify but may prove the most consequential. Consumer motivation is shifting. What began as a preference for understatement—”quiet luxury” as the shorthand—has evolved into something more substantive. Spending that once served as display is increasingly being redirected toward what might be called significant luxury: experiences oriented around health, knowledge, cultural engagement and emotional restoration. The question high-net-worth consumers are bringing to their spending decisions is no longer what this communicates about them, but what it actually does for them.

Trend One: From Wellness to Cognitive Longevity

The wellness narrative dominated luxury hospitality for the better part of a decade. Spa culture proliferated, meditation retreats entered the premium market and physical wellbeing became a credible status signal in its own right. What is emerging now is a more precise, more clinically informed iteration of that same impulse, one directed at the brain rather than the body.

Neurological performance, sleep optimisation, cognitive longevity programmes and neuro-aesthetic design are moving from the periphery of high-end hospitality toward its centre. According to CCL Hospitality’s Well-Being and Longevity 2026 Report, 83% of future luxury residents now consider mental fitness essential to their overall wellbeing. That figure is significant not because it confirms a trend that many operators already sense, but because it signals the speed at which mental performance has become a mainstream expectation rather than a niche offering.

For hotel groups and experiential operators, this requires more than a rebranding of existing programming. It demands genuine clinical and scientific expertise, a different vocabulary for describing outcomes and, critically, the ability to substantiate what is promised. Guests arriving with data from wearables and a working knowledge of sleep science are not a category that can be satisfied with incense and a sound bath. They are asking for measurable restoration, and they will know whether they received it.

Trend Two: Branded Ecosystems and the “Fourth Space”

The transactional stay of booked, enjoyed, departed, is giving way to something more continuous. Leading hospitality groups are building what some in the industry are beginning to describe as lifestyle ecosystems: integrated environments that combine branded residences, private members’ clubs, curated programming and ongoing community into a coherent whole. Knight Frank’s Residence Report 2025/26 documents strong demand amongst ultra-high-net-worth buyers for this model, specifically, permanent access to five-star services embedded into daily life, rather than reserved for annual travel.

The private members’ club was one of the more animated threads of the morning’s discussion, and it is not difficult to see why. The model works because it solves a problem that a well-appointed hotel room was never designed to address: the need for a framework of belonging. “Private members’ clubs create a sense of belonging,” one executive attending the BTB Breakfast Briefing observed. “They give people a network with structure. They create a world of their own.”

The question that follows is, how big do you want that world to be? The tension between the intimacy that makes a community meaningful and the scale that makes a business viable is real, and it is sharpening. The brands that are navigating it most convincingly are those building tiered architectures— close inner circles nested within broader ecosystems—that preserve genuine belonging at the centre without abandoning commercial ambition at the edges.

Trend Three: Return on Emotion

There is a growing body of evidence that luxury consumers are less interested in the physical room than in what surrounds it. Campaign‘s 2026 analysis found that 60% of luxury travellers now prioritise destination dining, cultural rituals and social experiences over the accommodation itself. The room, in this reading, has become infrastructure. The experience has become the product.

This shift from measuring success by occupancy and average spend to measuring it by the meaning and memory an experience generates is what some analysts are beginning to describe as a move from ROI to ROE, or Return on Emotion. It is a reframing that makes intuitive sense to guests and operational difficulty for brands, because emotional outcomes are harder to design for and harder to verify than physical ones.

The most direct challenge to emerge from the morning’s conversation came early, when a regional luxury hotel brand executive put the tension plainly: “We can only do so much. Yes, we can bring you awareness. We can explain our values, our proposition and evoke that desire to visit. Storytelling is one thing, but then it’s on the product to deliver.” It’s a straightforward observation, but one with real consequence for an industry that has become highly proficient at the language of transformation while sometimes struggling to operationalise it. The gap between a brand’s stated promise and a guest’s lived experience is not a communications problem. It is a product and people problem.

On people, the same executive was equally direct: “The people who represent the brand matter. They need to be intelligent psychologically. Put yourself in shoes of the person you want walking in to experience your luxury product or service. Also emotion doesn’t always mean purchase, but it starts the loop.” The point is not about training protocols or service standards, though those matter too. It is about the quality of human judgement in the moments that cannot be scripted, and the ability to read a guest’s state, to understand what they are actually seeking, and to respond in a way that feels considered rather than procedural. That capacity is not replicable by design or technology. It is, and will remain, a human one.

Trend Four: Liquid Luxury and Fractional Access

Gen Z and younger Millennials are approaching high-end consumption from a structurally different position to the generations that preceded them. Their preference is not for singular assets or permanent ownership, but for flexible, varied access—memberships and shared platforms that offer discovery, variety and social capital without long-term commitment. VML’s Future 100 Luxury Trends 2026 puts the global spending power of Gen Z alone approaching US$400 billion, with many in this cohort actively gravitating toward what the report describes as “brand democracies,” where co-creation and participation matter as much as the offer itself.

For operators, this is not merely a generational spending pattern to track. It’s a signal about the underlying logic of the luxury proposition and whether models built around permanence and singularity can continue to resonate with the cohort that holds the industry’s commercial future. Static propositions —a single property, a fixed membership tier, a non-negotiable ownership model—are already beginning to strain against the preferences of younger affluent consumers who have been conditioned by entirely different expectations of flexibility and access.

The more interesting strategic question raised in the room was not about product structure but about memory. Specifically: how does this generation actually retain and value an experience? The photograph, for years the defining currency of the shared luxury moment, is losing its authority. Not because experience matters less, but because the internal register of an experience is beginning to outweigh its external signal. “Does taking a photo on Instagram even still matter?” one agency executive asked. “Or have we reached the point where the memory you make for yourself is more valuable than the one you share?”

Trend Five: Cultural Stewardship and Regenerative Travel

The final shift is perhaps the most values-laden, and the one that brands are most at risk of mishandling. The language of sustainability has been so thoroughly absorbed into luxury marketing that it has lost much of its meaning. What is replacing it or rather, what is being demanded in its place, is something more active: regeneration. Not minimising negative impact, but demonstrating positive contribution to the cultural, environmental and community fabric of the places where these brands operate.

Regenera Luxury’s Tourism Evolution of 2026 research is instructive, finding that 80% of high-value consumers now favour brands positioned around regenerative impact over those still operating within a conventional sustainability framework. Legacy and cultural contribution are becoming markers of modern luxury in their own right, not additions to an ESG narrative, but central to how discerning consumers make decisions.

A luxury hotel auditor at some of the region’s most prestigious hotel groups framed the deeper challenge precisely: “You have to come back to the core question of: why is the brand doing it? That’s the question of subjectivity that most brands haven’t answered clearly enough for themselves, let alone for their guests.” The point applies with particular force to cultural stewardship. Brands that embed artists, chefs, local knowledge systems and community initiatives into their programming build a form of trust that is difficult to manufacture and almost impossible to replicate through aesthetics alone. Those that treat regeneration as a layer of communications rather than a genuine operating principle will, increasingly, be seen through by the very consumers they are trying to reach.

Experience: The Next Frontier

Taken together, the above trends leave little room for ambiguity: experience is the new currency of luxury. Not personalisation for its own sake, not curated aesthetics or algorithmically timed touchpoints, but something more grounded, values-driven, offline, and genuinely escapist in the sense that it removes a person from the noise of their ordinary life and returns them changed in some way that matters to them. The feeling, not the object, is what luxury consumers are now willing to pay for, and increasingly, it’s what they are demanding proof of before they do.

The brands that will thrive in this environment are those willing to build for that standard, investing in the purpose, the people and the depth of community required to deliver it consistently. Those that cannot will find that no price point, heritage narrative or five-star rating rescues a proposition that fails to produce the feeling it promises.

The BTB Breakfast Briefing is a six-weekly gathering of senior business and luxury leaders convened by Beyond the Boardroom, with insights from the sessions informing editorial coverage. Please contact BTB Events here for an invitation to our next session.