As Saks Global files for bankruptcy protection with over $2 billion in debt, the collapse of America’s most storied department stores signals not merely a business failure, but a fundamental transformation in how we’re understanding, consuming and valuing luxury itself. Can the modern department store revive itself from its gilded cage?

On Wednesday morning, Saks Global filed for Chapter 11 bankruptcy protection, bringing with it Saks Fifth Avenue, Neiman Marcus, and Bergdorf Goodman, names that have shaped American retail for over a century. The figures are sobering. More than $2 billion in debt, $100 million in missed interest payments, and nearly 17,000 employees whose futures now hang in the balance. Among the unsecured creditors are the luxury houses themselves: Chanel is owed approximately $136 million, Kering about $60 million, and Christian Louboutin $21.6 million, amongst others.

The immediate narrative appears straightforward enough. Saks acquired Neiman Marcus for $2.7 billion in 2024, betting that scale and consolidation would create operational efficiencies and strengthen negotiating power with luxury brands. Instead, the debt burden proved catastrophically unsustainable. When payments to vendors faltered, inventory shipments stopped, and empty shelves systematically eroded customer confidence. The cycle, once begun, proved impossible to arrest. Yet to understand this bankruptcy solely through the lens of financial miscalculation would be to miss the deeper transformation at work. What we’re witnessing is not simply the failure of one company but the conclusion of a particular chapter in how luxury has been discovered, desired, and acquired. The beloved department store model, for all its storied history and cultural significance, is now demonstrably at odds with the fundamental realities of contemporary retail.

Saks is hardly alone in this reckoning. The past five years have witnessed a devastating cascade of department store collapses across the globe. Robinsons in Singapore ended its 162-year history in 2020, closing its outlets at The Heeren and Raffles City, eventually re-emerging as an online-only operation—a fate shared by many of its contemporaries. Barneys New York filed for bankruptcy in 2019 after nearly a century in business, ultimately liquidating all its physical stores. In the UK, both Debenhams and House of Fraser collapsed into administration, whilst across Asia, Japanese retailers like Isetan shuttered multiple locations throughout Southeast Asia.

The pattern is unmistakable: department stores, regardless of their heritage or geographic location, are facing an existential crisis that transcends individual management failures or local market conditions.

To Market, To Market!

This decline has been building for years, driven by forces that have quietly but profoundly reconfigured the relationship between luxury brands and their traditional retail partners. Ralph Lauren now generates approximately two-thirds of its revenue through direct-to-consumer channels, a dramatic shift that would have been inconceivable two decades ago. Louis Vuitton, Chanel, and Gucci have invested billions in their own boutiques and digital platforms, fundamentally reorienting their distribution strategies. The reasoning is both economic and strategic: direct channels preserve significantly higher margins—department stores typically retain 40% to 50% of retail price—whilst also providing luxury houses with complete control over the customer experience and invaluable first-party data about purchasing patterns, preferences, and lifetime customer value.

This shift represents more than a mere redistribution of profit margins or a reallocation of retail real estate. When a luxury brand operates its own retail environment, it can orchestrate every element of the customer journey, from the atmosphere, lighting, and music to service standards and, most critically, the narrative framework within which its products are encountered and understood. It can ensure that its universe remains intact, hermetically sealed and undiluted by proximity to competing brands or conflicting aesthetics. The department store, by contrast, offers breadth and variety but necessarily compromises on the singularity of experience that contemporary luxury increasingly demands. In an attention economy characterised by fragmentation and sensory overload, that distinction permeates through to the consumer in more ways than one can reasonably underestimate.

The pandemic too, accelerated this transformation considerably, acting as a catalyst rather than a cause. As physical retail shuttered during lockdowns, luxury brands discovered that their own e-commerce platforms could sustain—and in many cases, dramatically expand—growth independently. Having made those substantial investments in digital infrastructure and established direct relationships with customers, the incentive to return to traditional wholesale arrangements has diminished substantially. Why cede margins and control when the alternative has proven not just viable but superior?

This structural shift coincides with a broader recalibration within the luxury market itself, one that challenges the industry’s post-pandemic assumptions about perpetual growth. According to Bain & Company, the global luxury consumer base has contracted from 400 million in 2022 to approximately 340 million in 2025, a startling reversal that represents not cyclical adjustment but structural change. Only about one-third of luxury brands experienced growth in 2024, a stark contrast to the 95% that saw expansion between 2021 and 2022. New customer acquisition has declined 5% year-over-year, suggesting that the pipeline of aspirational consumers has been severely constricted.

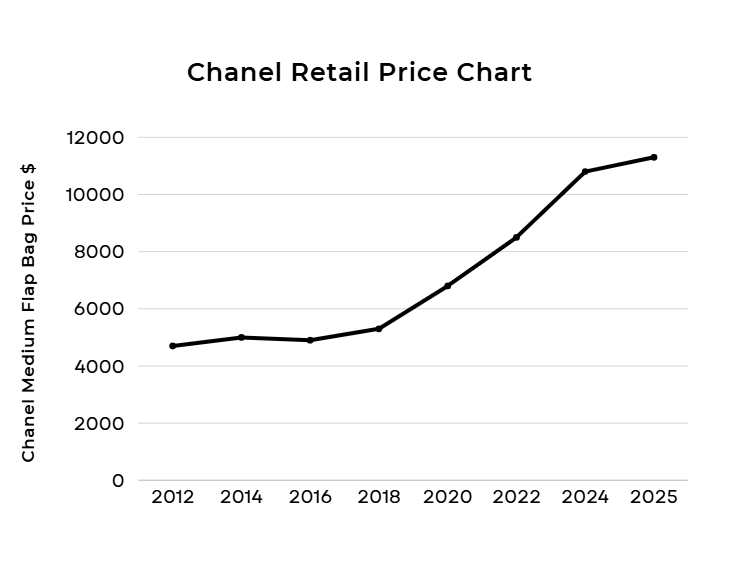

The industry’s aggressive pricing strategy over recent years, often justified as necessary to maintain exclusivity and brand positioning, has had profound and largely unintended consequences. A Chanel handbag that retailed for $3,180 in 2019 now commands $8,890, a price increase of nearly 180% that far outstrips inflation or any conceivable improvement in materials or craftsmanship. For middle-income consumers whose wages have remained relatively static, particularly in Western markets where income inequality has widened, these increases have placed aspirational luxury increasingly, and perhaps permanently, out of reach.

The aspirational consumer, once the foundation of accessible luxury’s growth and the demographic that sustained department stores’ luxury offerings, has largely withdrawn from the market, not by choice but by economic necessity.

Younger consumers, particularly Generation Z, approach luxury with notably different expectations and considerably more scepticism than their predecessors. Having grown up with unprecedented access to information and radical transparency about supply chains, manufacturing costs, and brand margins, they’re more inclined to question value propositions and far less susceptible to brand mystique alone. When TikTok videos can deconstruct exactly why a $500 T-shirt might be materially identical to a $50 alternative, the emperor’s new clothes become rather more visible. Social media has created both transparency about production realities and a fundamental shift in how status is signalled—increasingly through experiences, travel, and cultural capital rather than through possessions and logos.

The secondhand luxury market has flourished dramatically in this environment, creating a parallel economy that simultaneously democratises access and undermines the traditional luxury retail model. J.P. Morgan reports that 60% of US and European consumers now purchase pre-owned luxury goods through resale platforms, a figure that would have seemed unlikely a decade ago. This democratisation of access challenges both the exclusivity premium upon which luxury brands have historically traded and the economic model of new luxury retail. When a Hermès bag can be authenticated and acquired for 40% less on The RealReal, the department store’s full-price proposition becomes increasingly difficult to defend, particularly to a generation comfortable with circularity and suspicious of manufactured scarcity.

Can Geography Revive the Department Store?

Whilst American department stores have reduced their footprint over the last decade, further the Middle East has emerged as luxury’s strongest performing region, with growth projected at a robust 4% to 6%. The Middle Eastern retail market is expected to reach $1,532 billion by 2033, driven by robust tourism flows to Dubai and Abu Dhabi, and sustained domestic demand in markets like Saudi Arabia, where 25% of the population is under 14 and 62% under 30. This demographic dividend—young, digitally native consumers with rapidly growing disposable incomes and an appetite for luxury brands that hasn’t yet been exhausted by overexposure or cynicism—represents precisely what Western markets have lost.

The retail developments in these markets represent something fundamentally different from the tired shopping centres that characterise much of Western retail. These are destinations in themselves—significant spaces conceived by star architects that seamlessly integrate luxury retail with world-class dining, cultural programming, art installations, and entertainment. The Mall of the Emirates, Dubai Mall, and the forthcoming developments in Riyadh aren’t merely places to shop; they’re experiential destinations where the department store format continues to serve an essential function. It remains a place of discovery, of social occasion, of aspiration made tangible, not yet been displaced by the convenience of e-commerce and offering the physical embodiment of luxury as theatre.

Asian markets too, present a more nuanced and varied picture. Mainland China, once the engine of luxury growth, faces considerable headwinds, with luxury spending projected to contract by 3% to 5% as economic uncertainty and changing consumer sentiment dampen appetite for conspicuous consumption. The anti-corruption campaigns and cultural shifts towards more understated consumption have fundamentally altered purchasing patterns. Yet department stores in Japan and South Korea have demonstrated remarkable resilience by transforming themselves into something quite different from their Western counterparts. Japanese department stores like Takashimaya have become cultural institutions, hosting art exhibitions, offering cooking classes, and creating seasonal experiences that make them destinations rather than mere transactional spaces. They’ve grasped that in an age of infinite digital choice, physical retail must offer something irreducible, an experience that engages multiple senses, creates memories, and builds community.

The Gilded Cage

The path forward, if one exists, demands nothing short of radical reinvention. The department store of the future must offer experiences that cannot be replicated digitally—not pleasant shopping environments with a café tucked in the corner, but genuinely transformative encounters that justify both the journey and the premium. It must provide curation sharp enough to cut through the paralysis of infinite choice, offering genuine expertise and a distinctive point of view rather than mere product assortment. Service must transcend efficient transaction processing to become relationship-building that creates authentic loyalty and community. These spaces must function as destinations in the truest sense—places where people go not simply to acquire things but to be inspired, educated, and genuinely moved.

This represents an exceptionally high standard, one that demands both substantial capital investment and imaginative leadership willing to challenge every assumption about what retail can be. It remains genuinely uncertain how many institutions possess both the resources and imagination to achieve this transformation, particularly when burdened with legacy cost structures, debt loads, and decades of institutional inertia. The bar has been set, and it is formidably high.

The uncomfortable truth is that luxury is no longer anchored by the same certainties that sustained it for decades. Prestige, heritage and institutional authority still carry symbolic weight, but they’re no longer decisive on their own. For today’s consumer, value is increasingly personal, contextual and self-defined—less about inheriting a status and more about expressing a point of view. This shift leaves legacy players, particularly department stores, in a moment of reckoning. Their challenge is not competition on price, scale or convenience, but relevance. In a landscape where access is universal and choice is overwhelming, differentiation now lies in interpretation: the ability to edit, to guide, to create moments that feel considered rather than transactional.

Whether modern department stores can rediscover that capacity remains unresolved. But one thing is certain: the answer won’t be found in nostalgia or the assumption that a storied name guarantees a seat at the table. It will be defined by what luxury chooses to enable next, and whether it’s willing to become a partner in meaning-making rather than merely a purveyor of it. The gilded doors are closing. What replaces them will determine not just the future of retail, but what luxury itself means to a generation.